5 min read

Jan 15, 2025

State of Tokenized Private Credit

Written by

Nishikant Bahalkar

Share Now:

Tokenized private credit has rapidly grown to become the largest Real-World Asset (RWA) category after stablecoins, boasting $9.75 billion in active loans and $16.48 billion in total loans issued to date. This impressive growth signals that the market is not just a trend—it’s here to stay. To better understand how this sector is evolving, let’s dive into the data and uncover key insights driving its expansion. A special thanks to rwa.xyz for their outstanding analytics on tokenized private credit.

Let’s get started!

But before that, why tokenize private credit ?

Private credit provides attractive risk-adjusted yield opportunities for on-chain investors.

Tokenization simplifies access, allowing retail investors to tap into private credit markets that were once limited to institutional players.

Blockchain and smart contracts enhances transaction efficiency for the asset originators and investors by eliminating intermediaries. e.g 97% cost reduction for securitisation on centrifuge

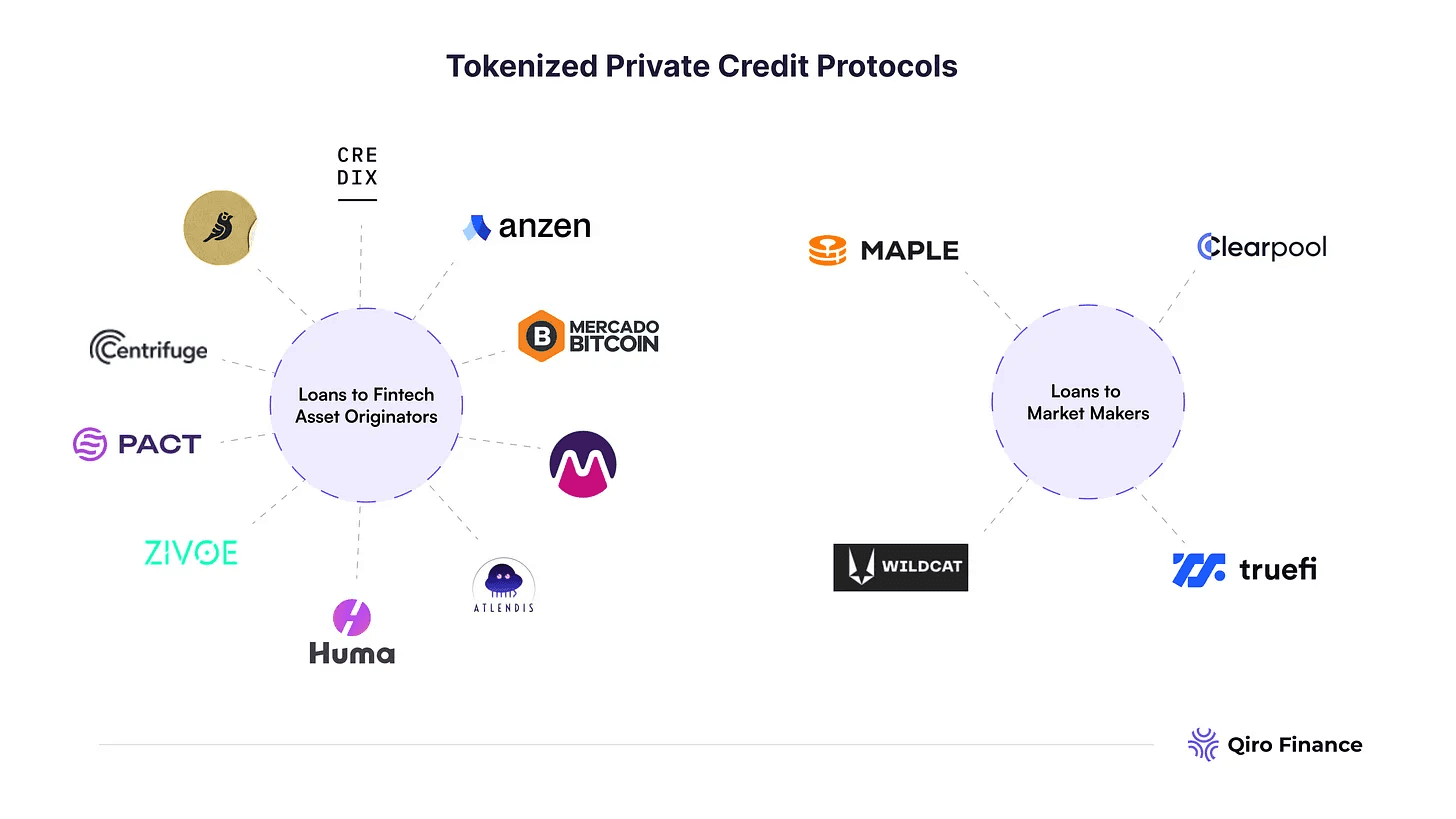

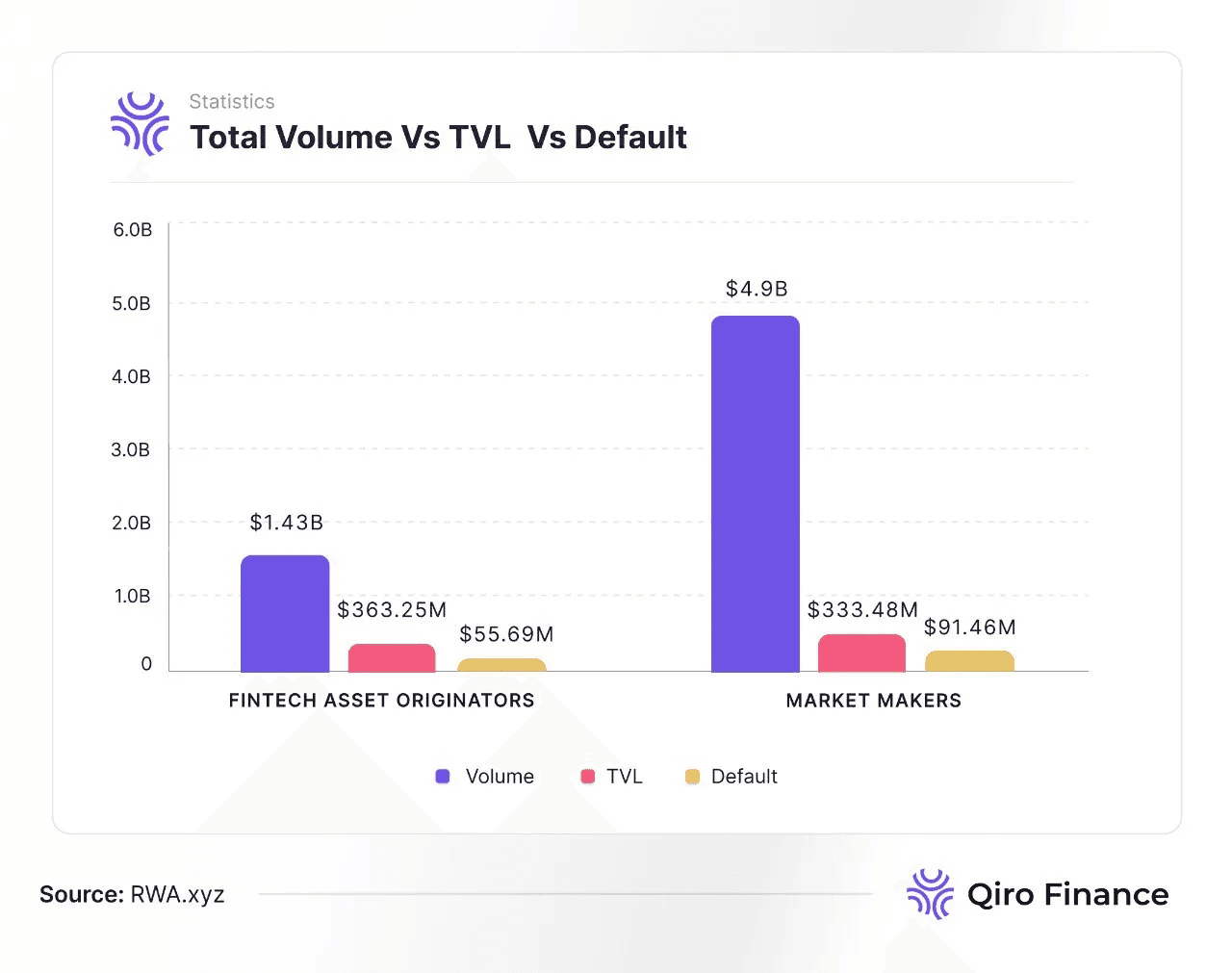

On a high level, there are two main categories in tokenized private credit protocols

1. Loans to fintech asset originators

This category involves real-world loans to non-crypto businesses like fintechs. These originators are lending companies/funds offering structured debt, real estate bridge loans, SME financing.

2. Loans to crypto market makers

Borrowers in this category generate revenue by trading or providing liquidity to crypto exchanges, their revenues are primarily driven by the crypto trading growth.

If we look at the distribution, market makers segment have achieved higher volumes compared to fintech, primarily driven by high volume short term loans. Most volume is from loans which were distributed to market makers in 2022 before FTX collapse.

However, fintech originator category has more active loans now attributed to recent growth of protocols

Active Loans

As of the end of 2024, private credit protocols hold $693.73 million in active loans. Notably, the market peaked at nearly $800 million in active loans in August 2024.

Maple Finance leads the sector with $269.6 million in active loans, solidifying its position as the largest private credit protocol. Following closely are Mercado Bitcoin and Centrifuge.

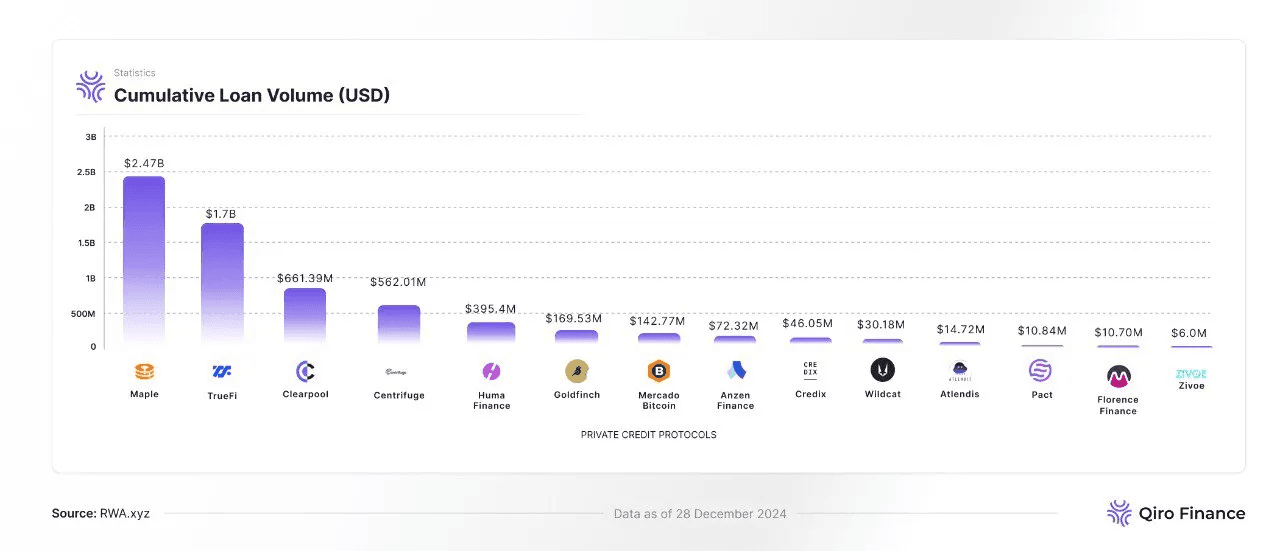

Loan Volume

Private credit protocols have issued a total of $6.31 billion in loans (excluding the $10.5 billion originated by Figure. The high loan volumes are largely driven by the top three protocols (Maple Finance, TrueFi & Clearpool), which primarily lend to market makers, explaining the higher loan volume.

In the fintech originators category, Centrifuge leads as the largest driver of loan volume, capitalizing on its institutional originator partnerships. Huma Finance follows closely, specializing in short-term payment financing and contributing notably to the sector's growth.

Chains

Despite its higher fees, Ethereum remains the primary blockchain for most leading private credit protocols, largely due to its deep stablecoin liquidity. Major players like Sky (formerly Maker) have been making private credit investments through platforms like Centrifuge, reinforcing Ethereum’s dominance in the space.

Emerging competitors are also gaining traction. Base, a newer entrant, has seen significant growth in active loans, driven primarily by Anzen, a stablecoin backed by private credit assets.

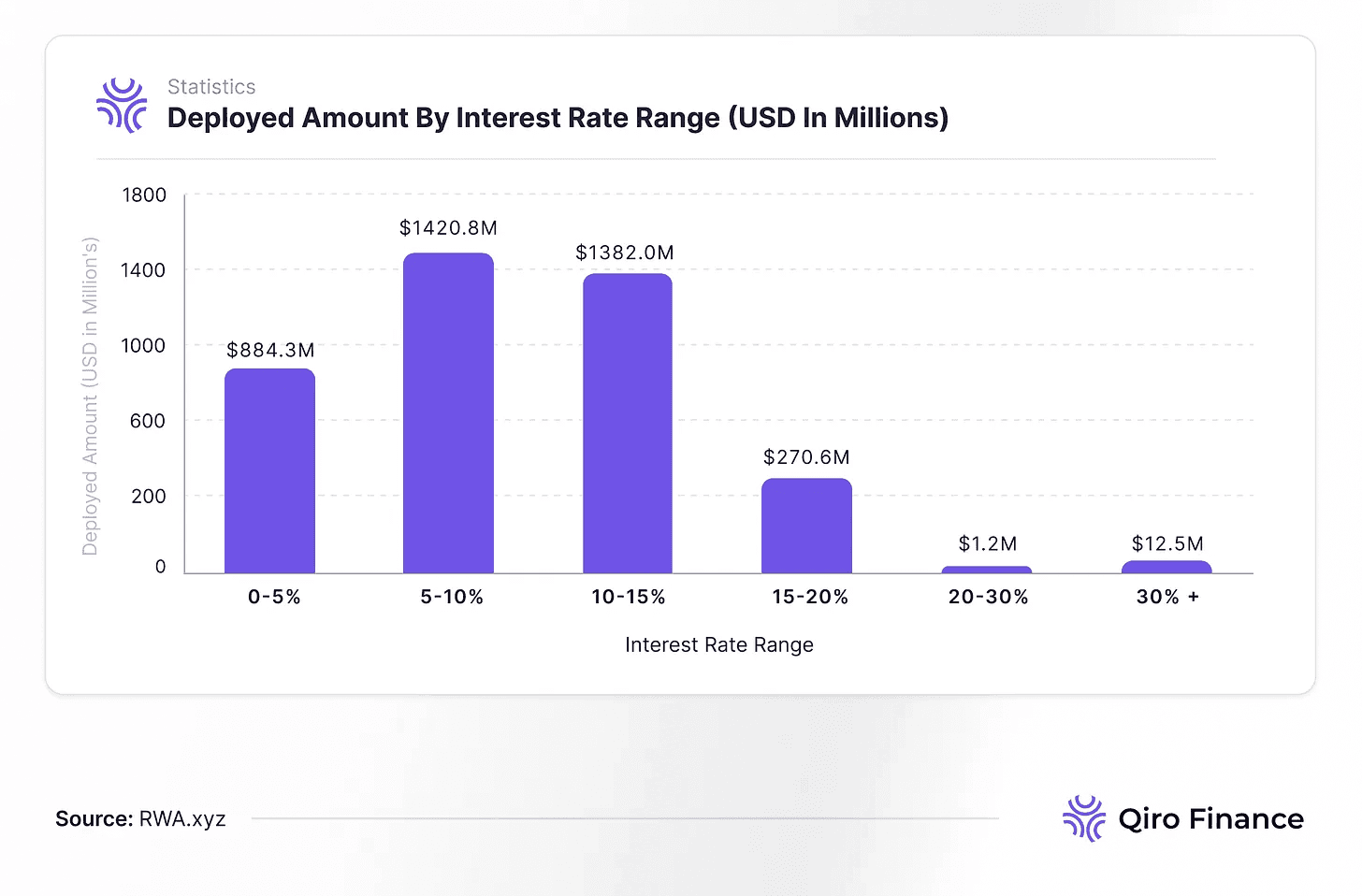

Yields

Most lending pools on private credit protocols primarily offer yields in the 5–15% range, with $1.42 billion deployed in the 5–10% bracket and $1.38 billion in the 10–15% range. This highlights a strong preference for moderate, risk-adjusted returns that are competitive with other on-chain lending markets.

While higher yields above 20% are less common, some protocols have achieved this through token rewards and incentives.

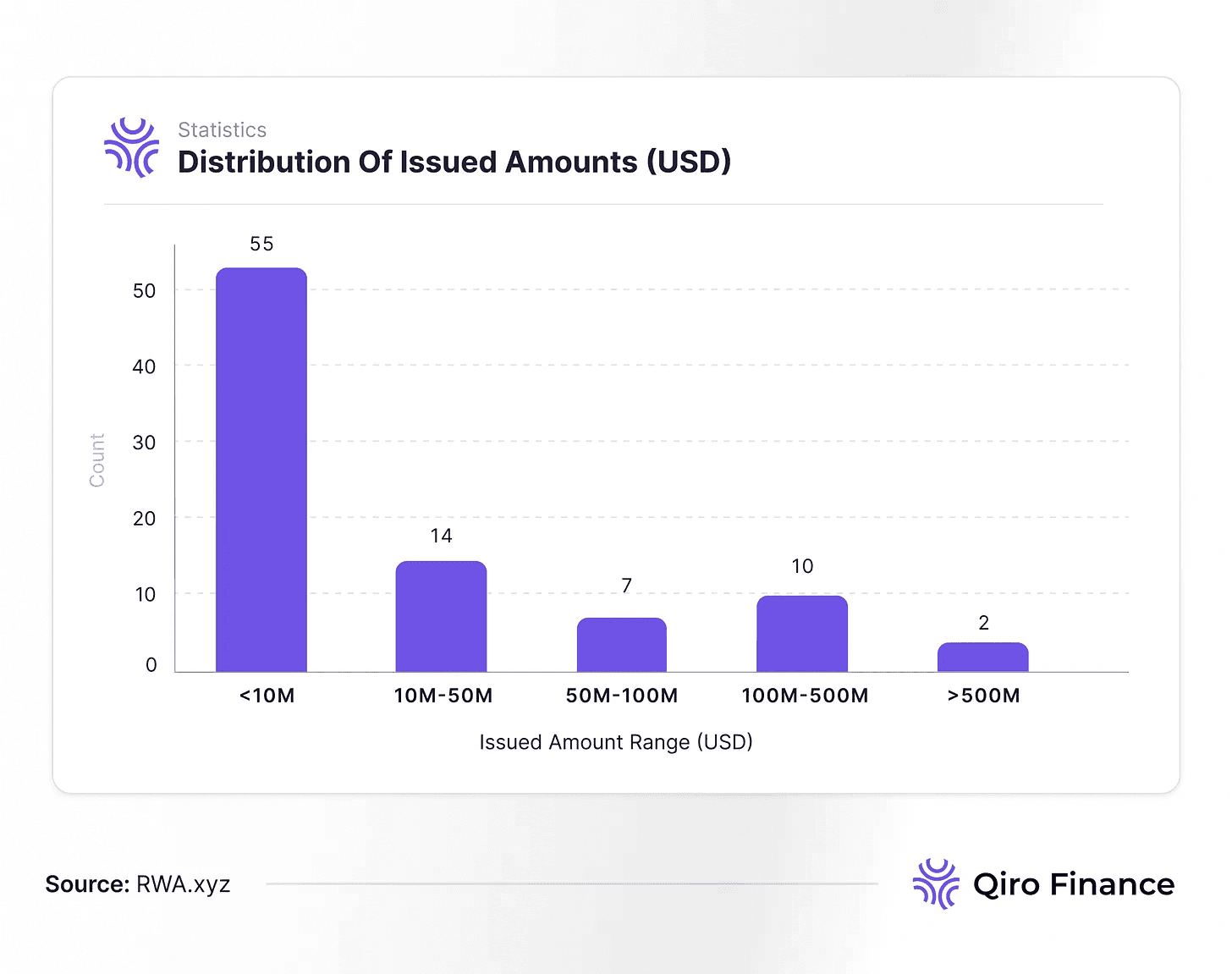

Lending Pool Size

Analyzing pool sizes reveals that most tokenized credit deals remain relatively small, typically under $10 million, reflecting the market's early stage. However, there are notable exceptions that showcase the potential for scale, such as Orthogonal Trading($580M) & M11 Credit Pool($550M) on Maple Finance, BlockTower Credit Pool($220M) on Centrifuge and Arf Financial Pool($295M) on Huma Finance which have facilitated larger loan volumes.

Note: single lending pool often consists of multiple underlying loans, allowing for diversified exposure even within smaller pools.

Distribution of Loan Volume (Pool level)

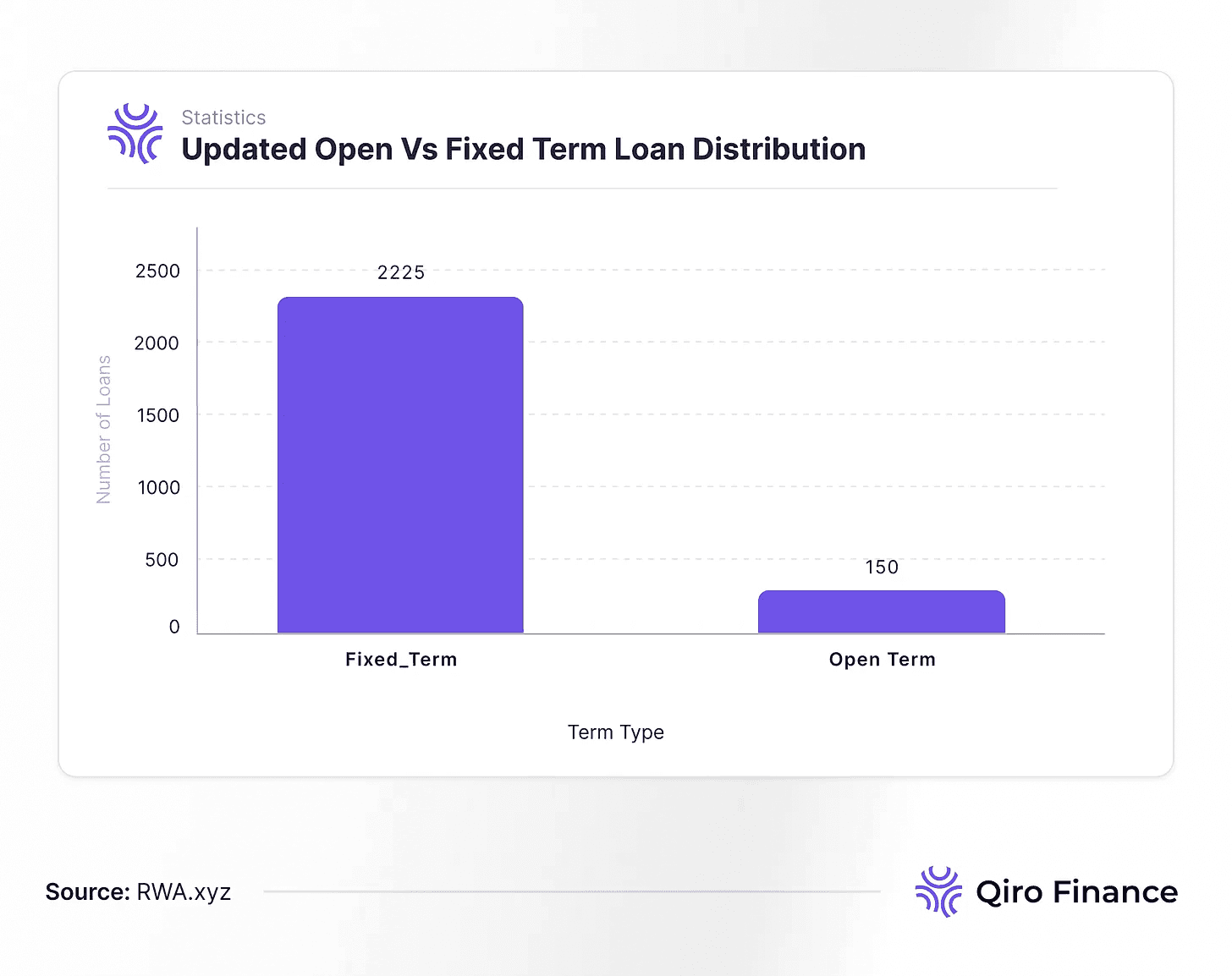

Loan Tenures

Fixed-term loans dominate the tokenized private credit market, accounting for approximately 94% of all loans, significantly outpacing open-term loans. Notably, around 68% of these fixed-term loans have tenures between 3–12 months, reflecting a strong preference for shorter durations. This trend likely stems from crypto investors' hesitation toward long lock-up periods, contrasting with traditional private credit markets where loan durations typically span 12–36 months

Loan Tenure was available only for 606 loans out of 2375

Repayment Type

Nearly 90% of loans on private credit platforms follow a bullet repayment structure, where borrowers make periodic interest payments and repay the entire principal in a lump sum at the end of the loan term. This structure keeps most cash flows locked until maturity, limiting interim liquidity for investors but providing borrowers with greater flexibility during the loan period.

Credit Defaults

Private credit protocols have faced $147.15 million in defaults, largely due to adverse selection and opaque underwriting practices, which have allowed lower-quality loans to enter the market. Instances of borrower misrepresentation have also contributed to significant losses, highlighting the need for more robust due diligence.

Additionally, defaults among market maker loans have been linked to broader macro events, such as the FTX collapse, underscoring the market's vulnerability to systemic shocks.

On-chain or off-chain, credit is credit, the quality of borrower remains of paramount importance. Qiro finance is working on this issue to improve state of underwriting in DeFi, with it’s distributed underwriting infrastructure.

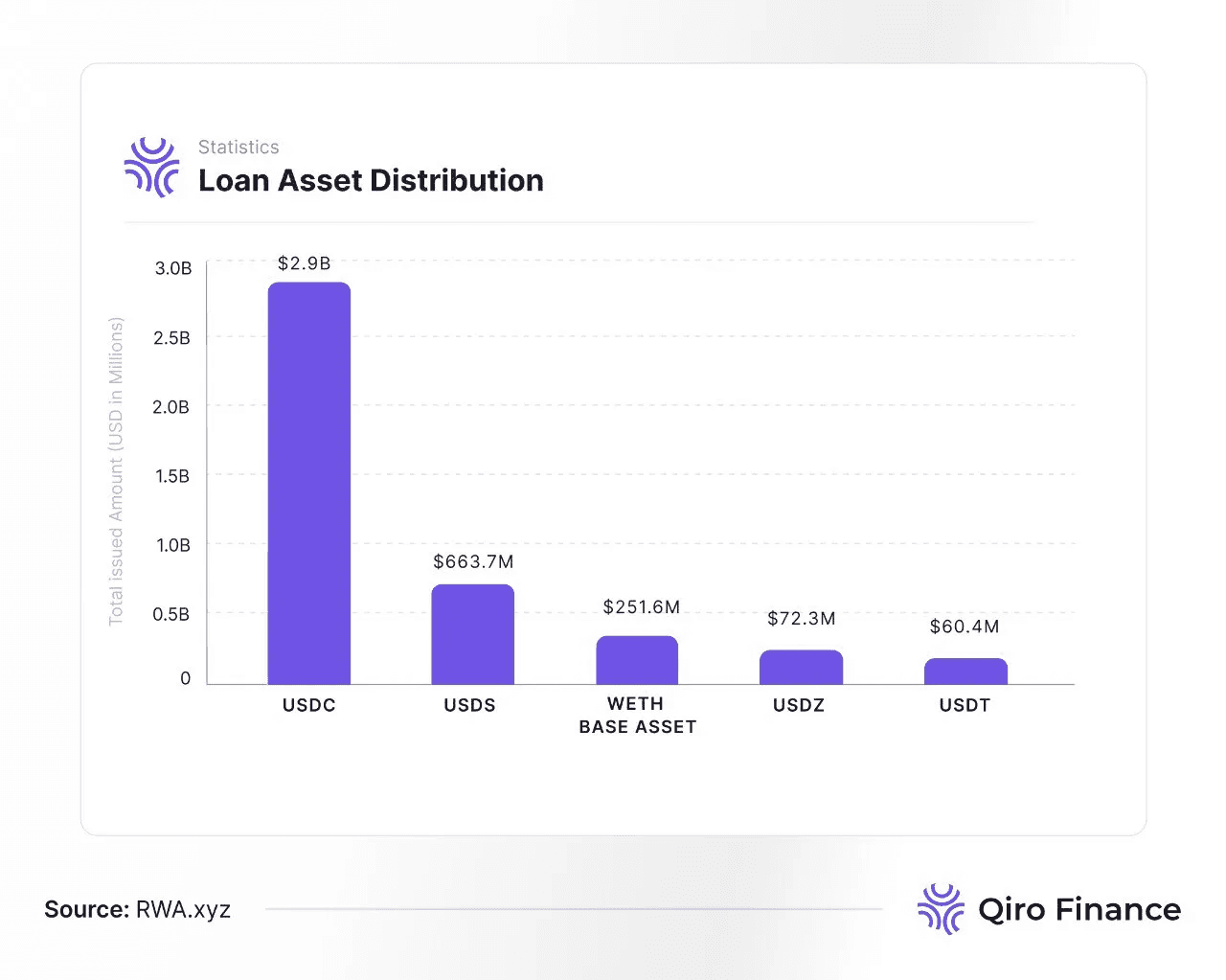

Loan Asset

USDC by Circle dominates the capital deployed in private credit protocols, largely driven by the issuer's focus on regulatory compliance. It is followed by USDS (formerly DAI), which has directly collateralized private credit assets to mint USDS, reflecting growing integration between stablecoins and real-world assets. In contrast, USDT has seen significantly lower participation in this sector. Additionally, some market maker loans are issued in wETH, totaling $251.6 million.

The rise of RWA-backed stablecoins is also notable, with Anzen emerging as a key player on Base, contributing $72.3 million in private credit-backed investments.

Region

While the broader thesis suggests that emerging market borrowers would dominate private credit platforms due to credit crunch in the region, the data tells a different story. The majority of loan volume to fintech originators is led by the USA, followed by Europe and the LATAM region. Although fintech originators in Asia and Africa are actively participating with numerous deals, their loan volumes remain relatively small compared to other regions.

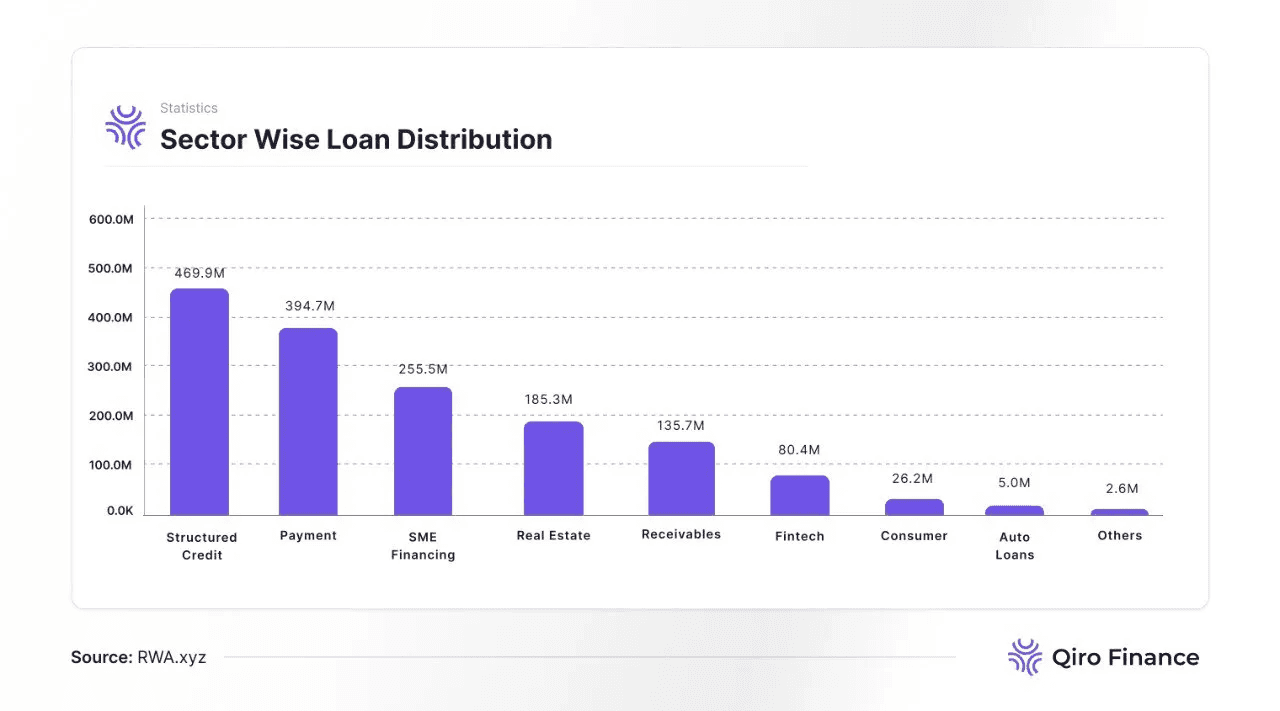

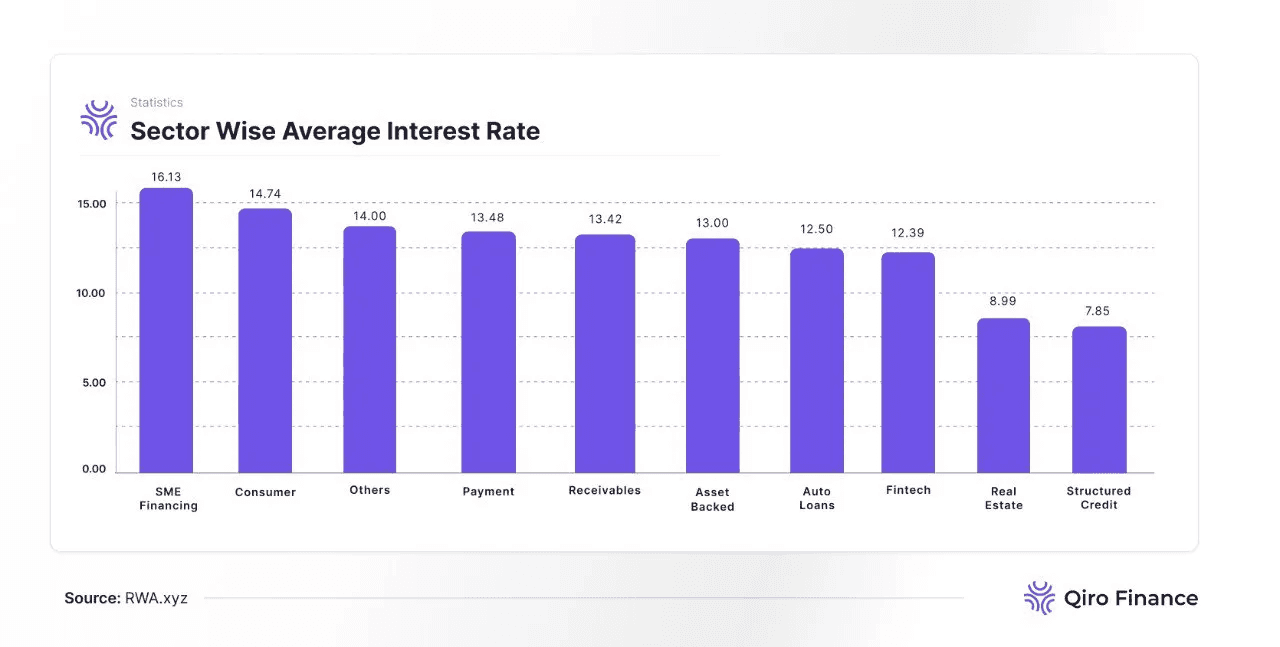

Sector

Although these platforms primarily focus on private credit, their lending pools are diversified across various sectors. Structured credit is a major focus area, with institutional players like BlockTower Capital issuing larger pools in this segment. Recently, payment financing has seen rapid growth, driven by leaders like Huma Finance, reflecting rising demand for short-term liquidity solutions.

Additionally, SME financing remains a key priority for many protocols due to its potential for higher yields and strong borrower demand, as small and medium-sized enterprises often face limited access to traditional financing options.

Key Drivers to supercharge the growth of Tokenized Private Credit in 2025 and Beyond

1. Improved credit underwriting/monitoring infra to avoid adverse selection(low quality loans) and credit defaults/losses.

2. Higher yield opportunities(~15%+) to make it attractive for investors.

3. Secondary markets enable investors to exit positions early, this can solve for the longer lockup issue.

4. Standardised and transparent risk assessment to make the products easier to understand for the broader investor base.

5. Clear regulatory structures to attract institutional capital allocators.

Looking Ahead

Tokenisation of private credit improves the $1.7T asset class with efficiency, transparency and accessibility unlocked with on-chain setup. With massive addressable market and attractive yield profile, it’s well positioned to become the leading RWA category in 2025.

Your scrollable content goes here